The headline S&P Global UK Construction Purchasing Managers’ Index (PMI) – a seasonally adjusted index tracking changes in total industry activity – posted 57.2 in September, up from 53.6 in August and above the neutral 50.0 threshold for the seventh successive month.

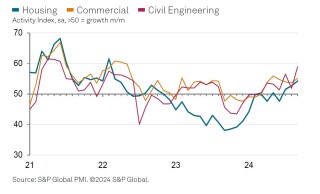

The survey suggests a strong upturn in total construction activity and the steepest rate of growth since April 2022. Civil engineering (index at 59.0) was the best-performing sub-sector but all three grew. Commercial building, at 55.2, had its highest score since May 2024 and house-building’s 54.3 was its highest since March 2022.

Total new orders expanded at the strongest rate for two-and-a-half years in September. Greater workloads encouraged additional staff recruitment, despite some firms noting that cost pressures had led to delays with the replacement of voluntary departures. Employment levels have now increased in four of the past five months.

Demand for construction products and materials meanwhile increased at a solid pace. The latest expansion of input buying was one of the fastest seen since early-2022. Suppliers’ delivery times nonetheless shortened again in September, which was linked to rising stocks among vendors. Some construction companies noted concerns about the outlook for steel prices and supply conditions due to recent closures of domestic blast furnaces.

Overall input prices increased for the ninth month running and at the steepest rate since May 2023. Construction companies commented on higher prices paid for a range of raw materials, as well as the pass-through of higher wages by suppliers.

Rates charged by subcontractors nonetheless increased only marginally and at the slowest pace so far in 2024.

Finally, business activity expectations for the year ahead remained upbeat in September despite slipping to the lowest since April. Optimism was often centred on prospects for sustained growth in the house building sector.

Tim Moore, economics director at S&P Global Market Intelligence, which compiles the survey, said: “UK construction companies indicated a decisive improvement in output growth momentum during September, driven by faster upturns across all three major categories of activity.

“A combination of lower interest rates, domestic economic stability and strong pipelines of infrastructure work have helped to boost order books in recent months.

“New project starts contributed to a moderate expansion of employment numbers and a faster rise in purchasing activity across the construction sector in September. However, greater demand for raw materials and the pass-through of higher wages by suppliers led to the steepest increase in input costs for 16 months.

“Business optimism edged down to the lowest since April, but remained much higher than the low point seen last October. Survey respondents cited rising sales enquires since the general election, as well as lower borrowing costs and the potential for stronger house building demand as factors supporting business activity expectations in September.”

Brian Smith, head of cost management at Aecom, said: “A seventh consecutive month of output growth is reflective of the surer footing the sector finds itself on, with the rate of inflation falling to more expected levels from the high rates seen over the last few years and developer confidence taking root since the spring.

“The sector will be intent on finishing the year well – boosted by government intervention in the planning system as its NPPF consultation comes to a close. Infrastructure and energy were major focuses of the Labour Party Conference. However, it remains to be seen how much the chancellor will be able to invest to stimulate the levels of renewal needed across the UK. The upcoming budget will therefore set the tone for development activity in 2025 and beyond.”