The advent of artificial intelligence (AI) has led to many companies claiming AI capabilities. Although not all of these are worthy AI investments, telecom giant Verizon Communications(NYSE: VZ) may be an overlooked sleeper AI stock.

AI darling Nvidia, for example, saw shares rise more than 130% over the past 12 months. Meanwhile, as recently as Jan. 10, Verizon shares hit a 52-week low of $37.59, and they remain near this low.

But how is Verizon contributing to the AI market’s expansion? Is it a buy with its share price down? Let’s dig into the company to address these questions.

Verizon contributes to the growth of the AI sector through its 5G wireless network. Its 5G service supports the fast speeds and security required to deliver AI to devices on the edge of a computer network, such as laptops and mobile phones.

An example of Verizon’s role in the AI edge computing space is its partnership with Nvidia to deliver AI to private networks, which are wireless services dedicated to specific organizations. For instance, Verizon will provide a private network to FIFA for the men’s 2026 World Cup.

According to CEO Hans Vestberg, “As we expand our 5G Ultra Wideband network and scale our private networks business, we’re opening up new opportunities for growth and innovation.”

Bringing AI to the edge positions Verizon to do just that. That’s because the AI edge computing sector is forecast to expand tenfold from $27 billion in 2024 to $270 billion by 2032. Delivering AI to the edge is key to facilitating the growth of self-driving cars, robotics, and the Internet of Things.

The company is currently growing revenue from its wireless services. In Q3, this part of Verizon’s business produced $19.8 billion in sales, a 3% year-over-year increase.

The growth of the AI edge computing industry is a promising tailwind for Verizon’s sales. However, other factors weigh on the company and, hence, its stock price.

While wireless service sales are growing, overall revenue is not. In Q3, total revenue of $33.3 billion was flat compared to 2023. The company’s revenue growth stalled as equipment sales fell year over year amid a macroeconomic environment of lower consumer discretionary spending.

Another factor is Verizon’s large debt burden. The telecom exited Q3 with over $150 billion in debt on its balance sheet. This debt could increase as the company prepares to acquire Frontier Communications Parent, a broadband internet service provider, in the coming months.

That said, the Frontier acquisition sets Verizon up to strengthen its rapidly growing broadband business, which also contributes to delivering AI to the edge. At the end of Q3, Verizon had total broadband connections of 12 million, representing 16% year-over-year growth. Acquiring Frontier will nearly double this by adding an estimated 10 million homes by 2026.

Although Verizon shoulders a large debt burden, the company benefits from the ability to generate strong free cash flow (FCF). FCF provides insight into the cash available to invest in the business, pay debt obligations, and fund dividends. The company’s Q3 FCF was $6 billion, bringing the year-to-date total to $14.5 billion.

This easily covered Verizon’s $8.4 billion in dividend payments made through the first nine months of 2024, leaving cash to pay down debt and support business growth. Dividends are a key reason to consider an investment in Verizon. The firm’s dividend yield is a staggering 7%. Also, Verizon raised its dividend for the 18th straight year in September. This long streak of increases, plus the telecom’s excellent FCF, means it’s a reliable source of passive income.

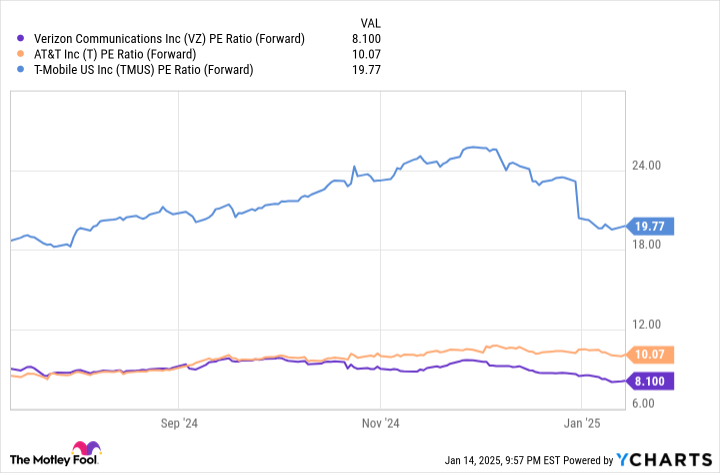

On top of that, Verizon reaching a 52-week low recently led to a forward price-to-earnings (P/E) ratio of eight. This metric helps to assess stock valuation by telling you how much investors are willing to pay for a dollar’s worth of earnings based on estimates for the next 12 months.

Data by YCharts.

Verizon’s forward P/E multiple is lower than that of its main rivals, AT&T and T-Mobile US. This suggests its stock is a better value than its competitors. Its low forward earnings multiple, coupled with a robust dividend, strong FCF, and a growing wireless service business, combine to make Verizon stock a buy.

Hold onto shares as a long-term investment to benefit from its dividend while the telecom titan tackles the growing AI edge computing market.

Before you buy stock in Verizon Communications, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Verizon Communications wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $843,960!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. TheStock Advisorservice has more than quadrupled the return of S&P 500 since 2002*.

See the 10 stocks »

*Stock Advisor returns as of January 13, 2025

Robert Izquierdo has positions in AT&T, Nvidia, T-Mobile US, and Verizon Communications. The Motley Fool has positions in and recommends Nvidia. The Motley Fool recommends T-Mobile US and Verizon Communications. The Motley Fool has a disclosure policy.

Is Verizon an Underappreciated Artificial Intelligence Stock to Buy in 2025? was originally published by The Motley Fool

Patricia Allen is a writer who loves to travel and explore new places. She's also passionate about fashion and style, so she often writes about cars and fashion on her blog.

She earned her degree in English Literature from Stanford University, where she studied under some of the most renowned writers of our time. After graduating, she moved to New York City to pursue her career as a writer. She has since written for several publications on topics ranging from arts to automotive news.