Costco Wholesale(NASDAQ: COST) is famous for several reasons. The big-box retailer is renowned for its low prices, vast product selection, and $1.50 hotdog meal combo, a favorite among shoppers that has remained the same price since its introduction in 1984.

The company is equally popular among investors. Late billionaire Charlie Munger, known most for his friendship and work alongside Warren Buffett, owned stock and served on the company’s board for years. Costco Wholesale has proven to be a tremendous investment, generating total returns exceeding 150,000% from the early 1980s.

It’s as strong a resume as you’ll find in a stock. But can investors count on Costco Wholesale moving forward? After all, past returns don’t guarantee future results.

Here is whether investors should buy Costco Wholesale stock right now.

The retail space is highly competitive. However, Costco Wholesale has carved out its niche as a leading big-box warehouse club retailer where consumers can buy things in bulk quantities but need a membership. It has nearly 900 warehouse stores worldwide, including 617 in the United States, and generated $264 billion in revenue over the past four quarters.

Costco’s business model is simple. It sells products at very thin margins and makes money on membership fees. Last quarter, Costco’s membership fees of $1.19 billion represented just 1.8% of total revenue but 51.5% of total operating income! Product selection, low prices, popular private-label brands, and quirky perks (the $1.50 hotdog) have translated to a sterling reputation that attracts shoppers.

In 2023, Axios ranked Costco as the second-most trusted U.S. company among consumers. Its brand power is so strong that Costco doesn’t spend money on advertising because it doesn’t need to, making it a formidable force in the retail space.

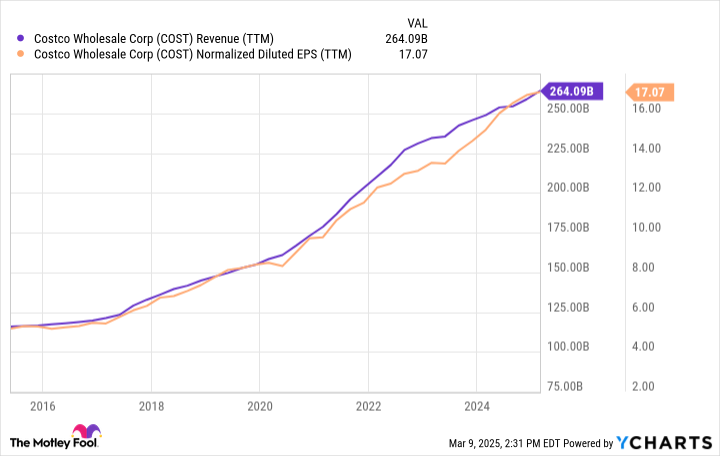

Costco’s customers are often high earners since buying in bulk can require spending large sums of money upfront. This demographic is lucrative because the top 10% of earners in America account for approximately half of all consumer spending. You can see that Costco’s top and bottom lines have grown without much interruption over the past decade, which goes a long way in explaining the stock’s stellar returns.

COST Revenue (TTM) data by YCharts

The cool part about Costco’s success is that it’s primarily organic. The company is growing because more people are shopping at Costco stores. Active warehouses have increased from 540 in 2010 to 897 today. Plus, years of inflation tack growth onto the business when you’re a cost leader selling goods at razor-thin markups. In other words, Costco grows as merchandise becomes more expensive over time.

It’s a similar story for Costco’s memberships, where volume drives revenue growth more than price increases. Paid memberships grew by 6.8% year over year last quarter. Costco did raise its membership fees late last year, but it was the first price hike in seven years. Today, a basic membership in the United States costs $65 (premium is $130) annually. That still seems reasonable and arguably leaves room for future price increases if needed.

Analysts estimate Costco will grow earnings by an average of about 9% annually, which seems realistic based on all these factors.

Looking at Costco’s past performance, business model, and growth opportunities, it’s probably evident that Costco Wholesale remains a top-notch stock worth adding to any long-term portfolio.

However, valuation is a wildcard that can stunt stock returns, even for the best companies. Unfortunately, Costco Wholesale is quite expensive today. At the time of this writing, the stock trades at a price-to-earnings ratio of 56, even after tumbling about 10% from its all-time high. I like using the PEG ratio (price/earnings-to-growth) to weigh a stock’s valuation against its anticipated growth. I’ll usually buy a high-quality stock with a PEG ratio of 2.0 to 2.5. The lower the ratio, the more value you’re getting. It gets increasingly difficult to justify buying stocks as you exceed that threshold.

Costco’s PEG ratio is 6.2, which is well beyond that. The stock could decline 50% from its current price and still be expensive.

Investors should jump on a chance to buy stock in Costco Wholesale, but not at this valuation. Consider waiting for a significant price decline or faster earnings growth to justify a higher valuation. Barring something unforeseen, it’s unlikely Costco Wholesale is a smart buy this month.

Before you buy stock in Costco Wholesale, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Costco Wholesale wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $745,726!*

Now, it’s worth notingStock Advisor’s total average return is830% — a market-crushing outperformance compared to164%for the S&P 500. Don’t miss out on the latest top 10 list, available when you joinStock Advisor.

See the 10 stocks »

*Stock Advisor returns as of March 14, 2025

Justin Pope has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Costco Wholesale. The Motley Fool has a disclosure policy.

Is Costco Stock a Buy in March 2025? was originally published by The Motley Fool

Patricia Allen is a writer who loves to travel and explore new places. She's also passionate about fashion and style, so she often writes about cars and fashion on her blog.

She earned her degree in English Literature from Stanford University, where she studied under some of the most renowned writers of our time. After graduating, she moved to New York City to pursue her career as a writer. She has since written for several publications on topics ranging from arts to automotive news.