Shares of both Palantir Technologies(NASDAQ: PLTR) and Nvidia(NASDAQ: NVDA) have delivered stunning gains this year thanks to the growing demand for both artificial intelligence (AI) hardware and software, though it is worth noting that one of these stocks has outperformed the other one by quite some distance.

Palantir stock’s gains of 345% (as of this writing) are significantly higher than the 188% jump that Nvidia has recorded this year. However, does this make Palantir the better AI stock to buy of the two? Let’s find out.

Nvidia may have made its name as the go-to provider of chips for companies looking to train AI models, but Palantir is the one that’s helping enterprises and governments bring those models into production. More importantly, the rapidly growing adoption of Palantir’s Artificial Intelligence Platform (AIP), which allows businesses to integrate large language models (LLMs) and generative AI into their operations, has led to a sharp acceleration in the company’s business and revenue pipeline.

Its revenue in the third quarter of 2024 was up 30% from the same period last year to $726 million. For comparison, Palantir’s top line increased at a much slower pace of 17% in 2023. The company’s growth has accelerated as the year has progressed, with Palantir management pointing out on the November earnings conference call that it “continues to see AIP-driven momentum both in expansions and new customer acquisitions.”

As it turns out, Palantir’s customer count swelled by a solid 39% year over year. Deal size also increased as the number of transactions worth at least $1 million increased by 30% year over year last quarter to 104.

The company isn’t attracting just new customers for its AI software platform; it is also winning more business from existing customers. This is evident from Palantir’s net-dollar retention rate of 118% in Q3, a metric that compares Palantir’s trailing-12-month revenue at the end of a quarter to the trailing-12-month revenue from the same customer cohort in the year-ago period. The company’s net dollar retention in the same quarter last year stood at 107%, suggesting that existing customers have increased their adoption of its platform.

Also, Palantir has a robust revenue pipeline that should allow it to sustain its impressive growth in the future as well. This is evident from the company’s remaining deal value (RDV) worth $4.5 billion, a metric that jumped 22% year over year in the previous quarter. The impressive growth in this metric bodes well for Palantir as RDV is the total remaining value of the company’s contracts at the end of a period.

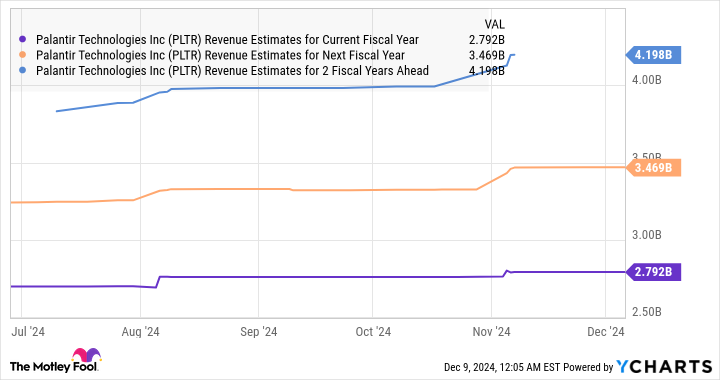

The above discussion tells us why Palantir has increased its full-year guidance, expecting just over $2.8 billion in revenue in 2024. That would be a 25% increase over 2023’s revenue of $2.23 billion. The estimates for the next two years have also been increased.

PLTR Revenue Estimates for Current Fiscal Year Chart

PLTR Revenue Estimates for Current Fiscal Year data by YCharts.

As the chart above shows, Palantir’s top line is expected to increase at 20%-plus rates over the next couple of years. However, don’t be surprised to see the company clocking stronger growth thanks to the massive opportunity in the AI software platforms market, a space that’s set to grow at an annual rate of close to 41% through 2028.

Palantir, therefore, has the potential to remain a top AI stock for a long time to come.

Nvidia stock’s returns this year pale in comparison to what Palantir has clocked, but investors shouldn’t forget the critical role that the company is playing in the proliferation of AI. The chipmaker reportedly controls more than 85% of the market for AI data center graphics processing units (GPUs), which explains why it has been clocking outstanding growth quarter after quarter.

NVDA Revenue (TTM) Chart

NVDA Revenue (TTM) data by YCharts.

What’s worth noting is that Nvidia’s dominance of the AI GPU market is so strong that rivals have been finding it difficult to make a dent in the company’s business. The company has reportedly sold out the entire capacity of its new Blackwell graphics cards for the next year, though the good part is that it is taking steps to ensure that it can increase supply.

Not surprisingly, Nvidia is expected to deliver another terrific year of growth in fiscal 2026 following a stellar show so far this year. Its revenue is expected to increase by 112% in fiscal 2025 to $129 billion, and the forecast for the next couple of years is quite robust as well.

NVDA Revenue Estimates for Current Fiscal Year Chart

NVDA Revenue Estimates for Current Fiscal Year data by YCharts.

Even better, Nvidia remains a top growth stock to buy for the long run even after the remarkable gains that it has clocked in the past couple of years. Catalysts such as the booming demand for AI chips and enterprise software, the transition to accelerated computing, the adoption of digital twins, and growing chip content in cars are the reasons why Nvidia may be sitting on a total addressable market worth a whopping $1.7 trillion.

It is also worth noting that Nvidia may become a threat to Palantir in the enterprise AI software space. CFO Colette Kress remarked on the company’s latest earnings conference call:

We expect Nvidia AI Enterprise full-year revenue to increase over 2x from last year, and our pipeline continues to build.

As such, Nvidia looks like a more complete AI stock as compared to Palantir. However, that’s not the only reason why it looks like the better AI pick of the two.

We have already seen that Nvidia is growing at a faster pace than Palantir. More importantly, Nvidia is expected to grow at a faster pace than Palantir in the next year despite being a much larger company. All this makes buying Nvidia stock over Palantir a no-brainer, especially after looking at the following chart.

PLTR PE Ratio Chart

PLTR PE Ratio data by YCharts.

Nvidia is significantly cheaper than Palantir despite enjoying superior growth. In fact, Palantir’s valuation is so rich that the stock’s 12-month median price target of $38 points toward a 50% drop from current levels. Nvidia, on the other hand, carries a 12-month median price target of $175, which would be a 23% increase from where it is now.

Moreover, Nvidia looks like the better AI stock to buy even for the long run considering that it addresses a much bigger addressable market thanks to its growing presence in AI software and dominance in hardware.

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

Nvidia:if you invested $1,000 when we doubled down in 2009,you’d have $350,239!*

Apple: if you invested $1,000 when we doubled down in 2008, you’d have $46,923!*

Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $492,562!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, and there may not be another chance like this anytime soon.

See 3 “Double Down” stocks »

*Stock Advisor returns as of December 9, 2024

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Nvidia and Palantir Technologies. The Motley Fool has a disclosure policy.

Better Artificial Intelligence Stock: Palantir vs. Nvidia was originally published by The Motley Fool

Patricia Allen is a writer who loves to travel and explore new places. She's also passionate about fashion and style, so she often writes about cars and fashion on her blog.

She earned her degree in English Literature from Stanford University, where she studied under some of the most renowned writers of our time. After graduating, she moved to New York City to pursue her career as a writer. She has since written for several publications on topics ranging from arts to automotive news.