Few stocks have taken investors on more of a roller-coaster ride in a single year than Super Micro Computer(NASDAQ: SMCI). At one point, the stock was up by as much as 318% from where it began 2024. Just a month ago, it was down by 36% year to date. Now, at the time of this writing, it’s up again by around 45% for the year.

The reasons behind those large movements actually were sound, considering what investors knew at the time. But now, investors want to know if Supermicro can regain the $118 high it reached earlier this year.

Start Your Mornings Smarter! Wake up with Breakfast news in your inbox every market day. Sign Up For Free »

Super Micro Computer has become a hot stock over the past few years because of its business. Similar to longtime artificial intelligence (AI) winner Nvidia (NASDAQ: NVDA), Supermicro makes components that go into powerful computing servers that train AI models. Supermicro also makes the components that allow a server to function, such as the physical racks and cooling infrastructure.

While not as high-margin as Nvidia’s GPUs, these are still necessary products, and Supermicro saw massive demand at the start of the year. This demand propelled its stock to lofty heights in March when it achieved the $118 per share stock price. However, this enthusiasm was too high, and Supermicro gradually sold off throughout the year as investors took profits.

The stock was still having a successful year until late August when Hindenburg Research published a short report alleging that Supermicro was engaging in some level of accounting fraud. To make matters worse, the following day, Supermicro announced it was delaying filing its end-of-year 10-K report to assess the “design and operating effectiveness of its internal controls over financial reporting.”

This kicked off the stock’s tumble, and further events — including the Department of Justice opening an investigation into the company and its auditor, Ernst & Young, resigning — made it seem like the stock was doomed. However, new information has caused the stock to recover significantly.

A special committee that included a member of Supermicro’s board, a legal team, and a forensic accounting team from Secretariat Advisors found no wrongdoing in accounting practices, although it did recommend replacing Supermicro’s CFO (a process that is currently ongoing). This news unwound basically all of the issues that drove Supermicro’s tumble over the past few months, but the stock is still well off its peak.

Investors hope for a more boring 2025 that’s dominated solely by business news, not allegations. So, is the stock worth buying now that it looks to be in the clear?

After Ernst & Young resigned, Supermicro brought on BDO, a top accounting firm. BDO still hasn’t certified Supermicro’s results from its fiscal 2025 first quarter, which ended Sept. 30, but it likely will do so soon.

Until then, we’ll have to rely on management’s preliminary results, which unfortunately aren’t good.

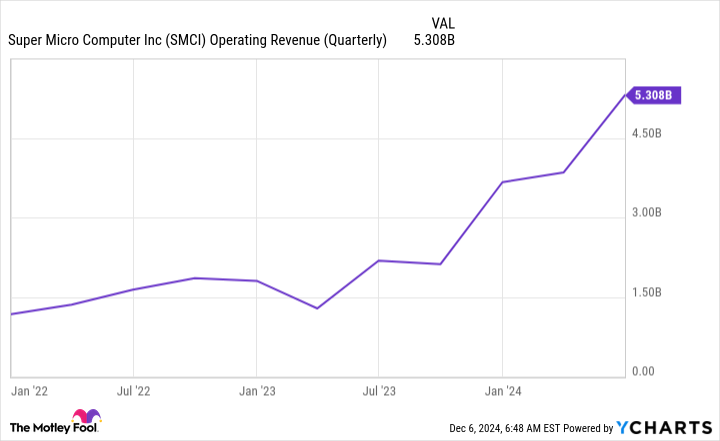

Supermicro had been guiding for fiscal Q1 revenue of $6 billion to $7 billion, but its preliminary results point to revenue actually landing between $5.9 billion and $6 billion. However, its preliminary EPS figures are near the middle of its guidance ranges, so the company’s profit picture is still intact.

SMCI Operating Revenue (Quarterly) data by YCharts.

For fiscal Q2, sales are expected to land between $5.5 billion and $6.1 billion. That would be a quarter-over-quarter decline, something that shouldn’t be happening considering that the AI market is still booming. One problem could be that Nvidia is allegedly shifting some orders for server hardware for its next-generation Blackwell GPUs away from Supermicro. That isn’t a good sign.

So, should investors open new positions in Supermicro after all that has gone on? I’d say no.

Even though management has taken the right steps to clear itself of accounting wrongdoing, there’s just no trust in the company. Additionally, with its revenues underperforming its guidance, there could be other turmoil within the company that is being overshadowed by the various ongoing investigations. (The Justice Department is still completing its probe.)

As a result, I’m avoiding the stock. There are far too many other good AI investments out there to waste my time with one that I cannot trust.

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

Nvidia:if you invested $1,000 when we doubled down in 2009,you’d have $369,349!*

Apple: if you invested $1,000 when we doubled down in 2008, you’d have $45,990!*

Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $504,097!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, and there may not be another chance like this anytime soon.

See 3 “Double Down” stocks »

*Stock Advisor returns as of December 9, 2024

Keithen Drury has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Nvidia. The Motley Fool has a disclosure policy.

Is Super Micro Computer Set for a Comeback in 2025? was originally published by The Motley Fool

Patricia Allen is a writer who loves to travel and explore new places. She's also passionate about fashion and style, so she often writes about cars and fashion on her blog.

She earned her degree in English Literature from Stanford University, where she studied under some of the most renowned writers of our time. After graduating, she moved to New York City to pursue her career as a writer. She has since written for several publications on topics ranging from arts to automotive news.